Incident response in banking ISMS is the systematic process that enables financial institutions to detect, contain, and recover from cybersecurity and operational incidents while satisfying regulatory requirements under ISO 27001:2022, EU DORA, and U.S. frameworks including FDIC and NYDFS rules. The role of incident response in banking ISMS extends well beyond technical remediation. It generates the evidentiary record that supervisors examine during audits, supports board-level risk reporting, and determines whether a bank can safely pursue digital modernization without triggering regulatory intervention. Banks that treat incident response as a compliance checkbox rather than an operational capability consistently face examination findings that more mature peers avoid.

How incident response integrates with ISO 27001 and banking regulations

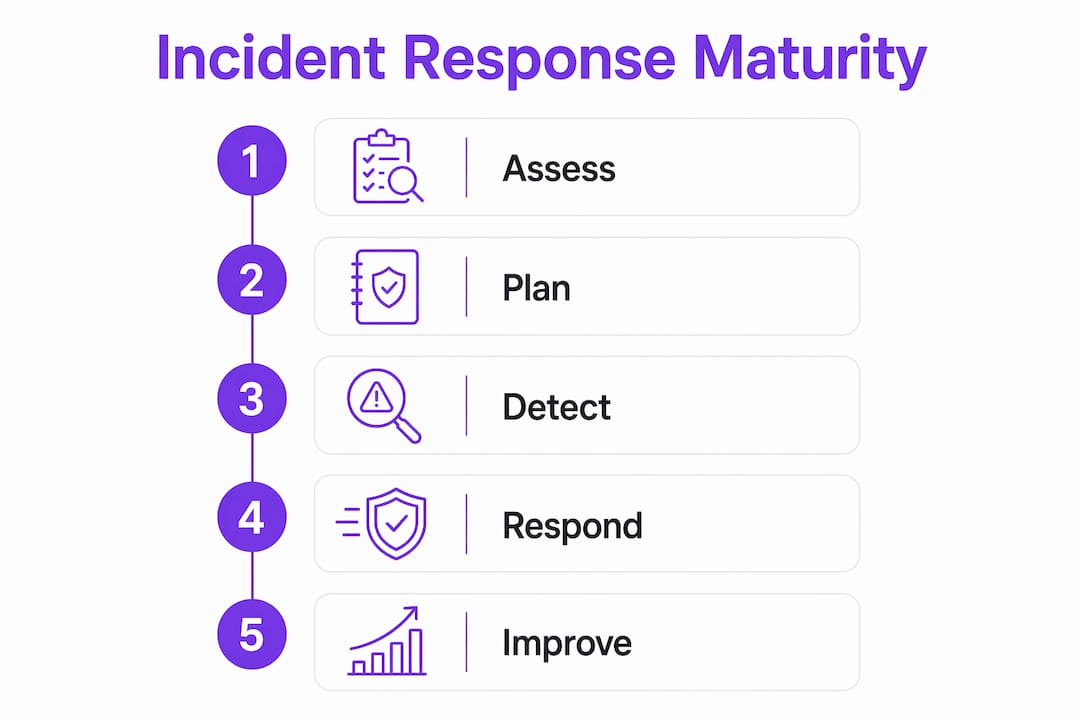

ISO 27001:2022 controls A.5.24 through A.5.27 form the direct regulatory spine of incident management in financial institutions. Control A.5.24 requires planning and preparation. A.5.25 covers assessment and decision-making. A.5.26 addresses response to incidents. A.5.27 mandates post-incident learning and improvement. Together, these controls create a closed loop that regulators can audit from end to end.

The overlap between ISO 27001:2022 and EU DORA is substantial. EU DORA and ISO 27001:2022 share incident reporting requirements, meaning banks that maintain a certified ISMS can use that documentation directly as audit evidence under DORA mandates. That alignment reduces audit friction and avoids duplicate documentation efforts across regulatory regimes.

Notification timelines add another layer of operational pressure. Banks face 36-hour notification windows for federal regulators and 72-hour windows under NYDFS for cybersecurity incidents. Missing these deadlines is itself an examination finding, independent of the incident’s technical severity. That reality makes detection speed and escalation clarity non-negotiable operational requirements, not aspirational goals.

| Regulatory framework | Notification timeline | Key requirement |

|---|---|---|

| FDIC / OCC / Federal Reserve | 36 hours | Notify federal banking agencies of significant incidents |

| NYDFS Part 500 | 72 hours | Report cybersecurity events to the Department of Financial Services |

| EU DORA | 4 hours (initial) / 72 hours (intermediate) | Tiered reporting for major ICT-related incidents |

| ISO 27001:2022 | Defined by ISMS policy | Document, assess, and respond per A.5.24–A.5.27 controls |

A certified ISO 27001 ISMS also gives CISOs a common language for communicating cybersecurity risks and resource needs to boards. That shared vocabulary matters when securing budget for incident response improvements before an incident occurs.

What does effective incident response execution look like in banking?

ISO 27001 incident management requires a tiered response structure that prioritizes incidents by severity and mandates cross-functional coordination. Effective execution depends on clearly defined roles, tested escalation paths, and documented communication workflows. Without these, even technically capable teams lose time during real incidents while determining who owns each decision.

Role-based responsibilities are the foundation. Every incident response plan in a banking ISMS should assign specific individuals to detection, triage, containment, communication, and recovery. On-call escalation matrices must be current, tested, and accessible outside normal working hours. A plan that lists names without contact details and backup contacts is not a plan. It is a liability.

Communication is where most banking incident response programs fail under pressure. A critical and often overlooked requirement is out-of-band emergency communication. When internal email, Slack, or Teams channels are compromised or unavailable during an incident, teams need a separate, secure, two-way communication system with off-network access. This system must support location targeting and acknowledgment confirmation so incident commanders know who has received critical instructions.

Key elements of a banking incident response execution framework:

- Severity classification criteria: Written thresholds that define what constitutes a P1, P2, or P3 incident, with examples specific to banking operations such as core banking outages, wire transfer fraud, and data exfiltration.

- Escalation matrix: Named roles with primary and backup contacts, including legal, compliance, and communications teams alongside IT and security.

- Out-of-band communication channel: A secure, off-network system for crisis coordination when primary channels fail.

- Evidence capture protocol: Real-time logging of decisions, severity determinations, and communications throughout the incident lifecycle.

- Regulatory notification triggers: Documented criteria that automatically initiate the 36-hour or 72-hour notification clock.

Pro Tip: Document the rationale behind every severity determination during an incident, not just the outcome. Regulators examine why a bank classified an event as minor. A missing justification is as damaging as the wrong classification.

How do banks measure and improve incident response maturity?

Incident response maturity functions as an operational feasibility constraint in banking. It determines whether a bank can safely pursue digital channel expansion, cloud migration, or third-party integrations without creating supervisory risk. A bank with immature detection and containment capabilities that launches a new mobile banking platform is not taking a calculated risk. It is creating an uncontrolled one.

ISO 27001 requires annual testing of incident response capabilities. The standard calls for realistic tabletop exercises that simulate threats relevant to banking operations. Common scenarios include point-of-sale breaches, business email compromise, ransomware affecting core banking systems, and third-party vendor failures. These exercises reveal coordination gaps that no policy document can expose.

Common deficiencies that tabletop exercises surface in banking environments:

- Unclear escalation ownership: Teams disagree in real time about who has authority to declare a major incident or initiate regulatory notification.

- Inadequate system isolation procedures: Containment steps exist on paper but have never been tested against production-equivalent environments, creating uncertainty about service disruption risk.

- Missing regulatory notification triggers: Teams cannot identify the precise moment the 36-hour or 72-hour clock starts, leading to late notifications.

- Outdated contact information: Escalation matrices reference former employees or stale phone numbers discovered only during the exercise.

- Insufficient evidence capture: Teams focus on technical remediation and produce no contemporaneous record of decisions, making post-incident regulatory review difficult.

Remediation follows a straightforward priority order. Fix escalation clarity first because it unblocks every other response action. Update contact information quarterly, not annually. Test isolation procedures in a staging environment before the next tabletop. Build notification triggers into your incident tracking system so the clock starts automatically when severity thresholds are met.

Board-level metrics for incident response maturity include mean time to detect, mean time to contain, exercise frequency, remediation closure rates, and evidence quality scores. These metrics connect cyber investment to resilience outcomes. Boards that review control inventories instead of these operational metrics are measuring the wrong things.

Pro Tip: Run at least one unannounced tabletop exercise per year. Announced exercises test your plan. Unannounced exercises test your actual capability. Regulators know the difference, and so do examiners reviewing your exercise logs.

What is an incident action plan, and why do banking regulators care?

An incident action plan (IAP) is a per-incident document that defines objectives, resource assignments, timelines, and communication responsibilities for a specific event. It differs from a standing incident response plan, which is the permanent policy document. The IAP is the operational playbook for a single incident. The standing plan is the framework that governs all incidents.

| Document | Purpose | Scope | Regulatory expectation |

|---|---|---|---|

| Standing IR plan | Governs all incidents | Permanent, policy-level | Required by ISO 27001, OCC, FDIC, Federal Reserve |

| Incident action plan (IAP) | Manages a specific incident | Per-event, operational | Expected as evidence of structured response |

Well-documented IAPs satisfy regulatory expectations from the OCC, FDIC, and Federal Reserve. Regulators do not mandate a specific IAP format, but they expect evidence of structured operational risk management. An IAP that documents objectives, assigned resources, decision timelines, and communication logs provides exactly that evidence. A bank that responds to a major incident without producing an IAP creates an evidence gap that examiners will flag.

The key elements of an effective banking IAP are objectives stated in plain language, resource assignments with named individuals and their specific responsibilities, a timeline that records when each action was taken and by whom, and a communication log that captures every internal and external notification. For ISO 27001 audit preparation, the IAP becomes a primary evidence artifact demonstrating that the bank’s ISMS controls functioned as designed during a real event.

The primary value of incident response documentation in banking is evidentiary. Capturing the rationale behind decisions prevents examination findings during post-incident reviews. A bank that can show an examiner a complete IAP with timestamped decisions, severity justifications, and notification records is in a fundamentally different position than one that can only describe what happened verbally. For guidance on avoiding common pitfalls in this area, the ISO 27001 finance implementation mistakes resource covers the documentation failures that most frequently trigger findings.

Key Takeaways

Incident response maturity in banking ISMS is both a regulatory requirement and the operational foundation that determines whether digital transformation is safe to pursue.

| Point | Details |

|---|---|

| ISO 27001 controls A.5.24–A.5.27 | These four controls define the full incident management lifecycle banks must implement and evidence. |

| Notification timelines are hard deadlines | FDIC requires 36-hour notification; NYDFS requires 72 hours. Missing either is an independent examination finding. |

| Out-of-band communication is non-negotiable | Banks need a secure, off-network communication system for incidents that compromise internal channels. |

| IAPs are the primary audit evidence | Per-incident action plans with timestamped decisions satisfy OCC, FDIC, and Federal Reserve expectations. |

| Maturity metrics belong in board reports | Mean time to detect and contain, exercise frequency, and evidence quality connect cyber spend to resilience outcomes. |

Why incident response maturity is the real constraint on digital banking growth

Banks talk about digital transformation as a growth strategy. I think about it differently. Incident response maturity is the actual constraint on how fast a bank can safely modernize. Every new digital channel, every cloud migration, every third-party API integration expands the attack surface. If your detection, containment, and recovery capabilities cannot keep pace with that expansion, you are not transforming. You are accumulating unpriced risk.

The regulatory timeline pressure makes this concrete. A bank that cannot reliably detect a significant incident within hours of occurrence cannot meet a 36-hour federal notification requirement. That is not a theoretical gap. It is a supervisory intervention waiting to happen. I have seen institutions invest heavily in new product launches while their incident response programs still relied on internal email for crisis communication and annual tabletop exercises that everyone knew were coming.

The fix is not complicated, but it requires leadership attention that most banks redirect toward revenue-generating initiatives. Alternate communication channels, detailed decision logs, quarterly contact verification, and unannounced exercises are not glamorous investments. They are the difference between a bank that handles its next major incident with confidence and one that spends the following six months responding to examiner requests.

Boards that focus on resilience metrics rather than control inventories make better decisions about digital risk tolerance. Mean time to contain is a more honest measure of readiness than a list of policies. If you are a compliance officer or IT manager reading this, that framing is worth bringing to your next board presentation.

— Martin

Ismscalculator tools for banking ISMS and incident response readiness

Banking professionals who need a clear picture of their ISO 27001 readiness before the next examination cycle can use Ismscalculator to get there faster.

The ISO 27001 readiness assessment from Ismscalculator benchmarks your incident response maturity across all 14 ISO domains, including the A.5.24–A.5.27 controls most relevant to banking operations. The platform delivers tailored estimates based on your institution’s size, industry, and current security maturity. For teams that need a faster starting point, the 2-minute self-assessment provides an immediate baseline. Banks that need implementation support can connect with vetted ISO 27001 consultants through the platform to accelerate their path to certification and supervisory confidence.

FAQ

What is the role of incident response in banking ISMS?

Incident response in banking ISMS is the structured process for detecting, managing, and recovering from cybersecurity and operational incidents while generating the evidentiary record regulators require. ISO 27001:2022 controls A.5.24 through A.5.27 define the specific requirements banks must implement and document.

How does EU DORA relate to ISO 27001 incident management?

EU DORA and ISO 27001:2022 share overlapping incident reporting requirements, so banks with a certified ISMS can use that documentation directly as audit evidence under DORA. This alignment reduces duplicate compliance work and lowers audit friction for financial institutions operating across EU jurisdictions.

What notification timelines do U.S. banks face for cybersecurity incidents?

U.S. banks must notify federal banking agencies within 36 hours of a significant incident and must report to NYDFS within 72 hours under Part 500. Missing either deadline is an independent examination finding, regardless of how well the bank managed the incident technically.

What is an incident action plan in banking?

An incident action plan is a per-incident document that defines objectives, resource assignments, timelines, and communication logs for a specific event. Well-documented IAPs satisfy OCC, FDIC, and Federal Reserve expectations for structured operational risk management during cybersecurity events.

How often should banks test their incident response capabilities?

ISO 27001 requires annual testing through realistic tabletop exercises simulating threats relevant to banking operations, such as ransomware, business email compromise, and third-party vendor failures. Running at least one unannounced exercise per year provides a more accurate measure of actual capability than announced drills alone.